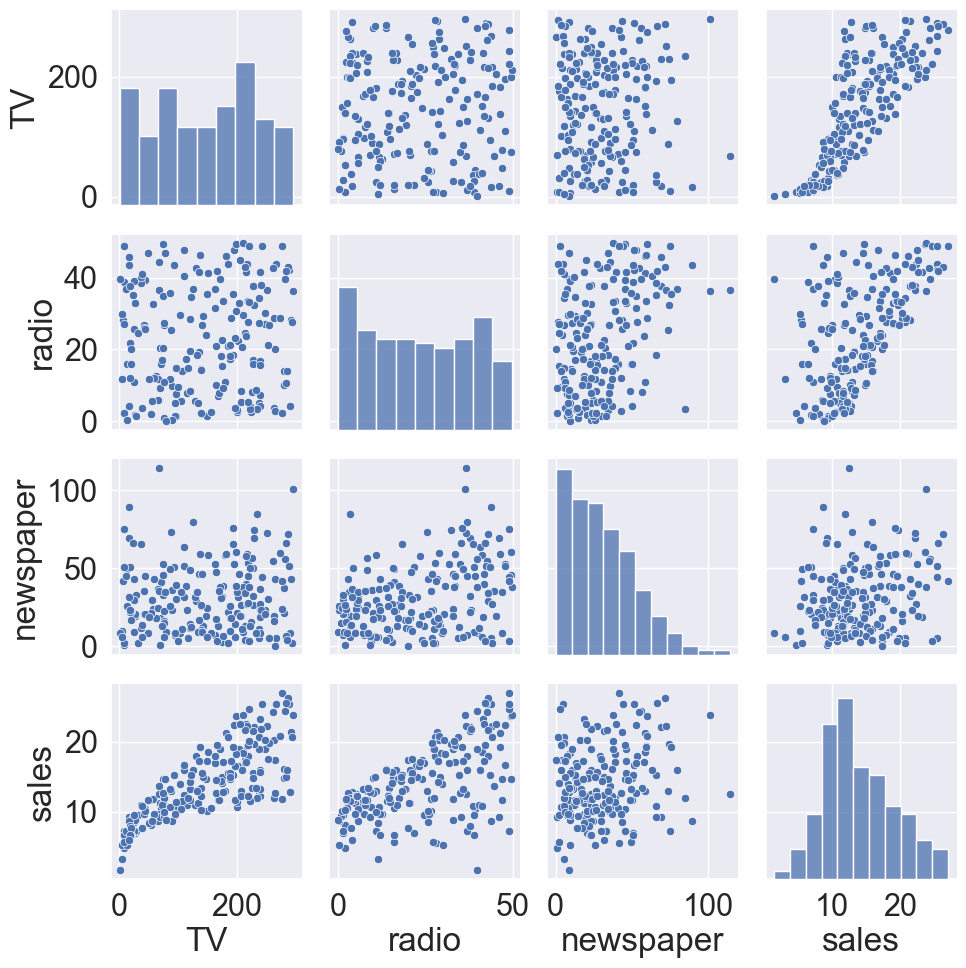

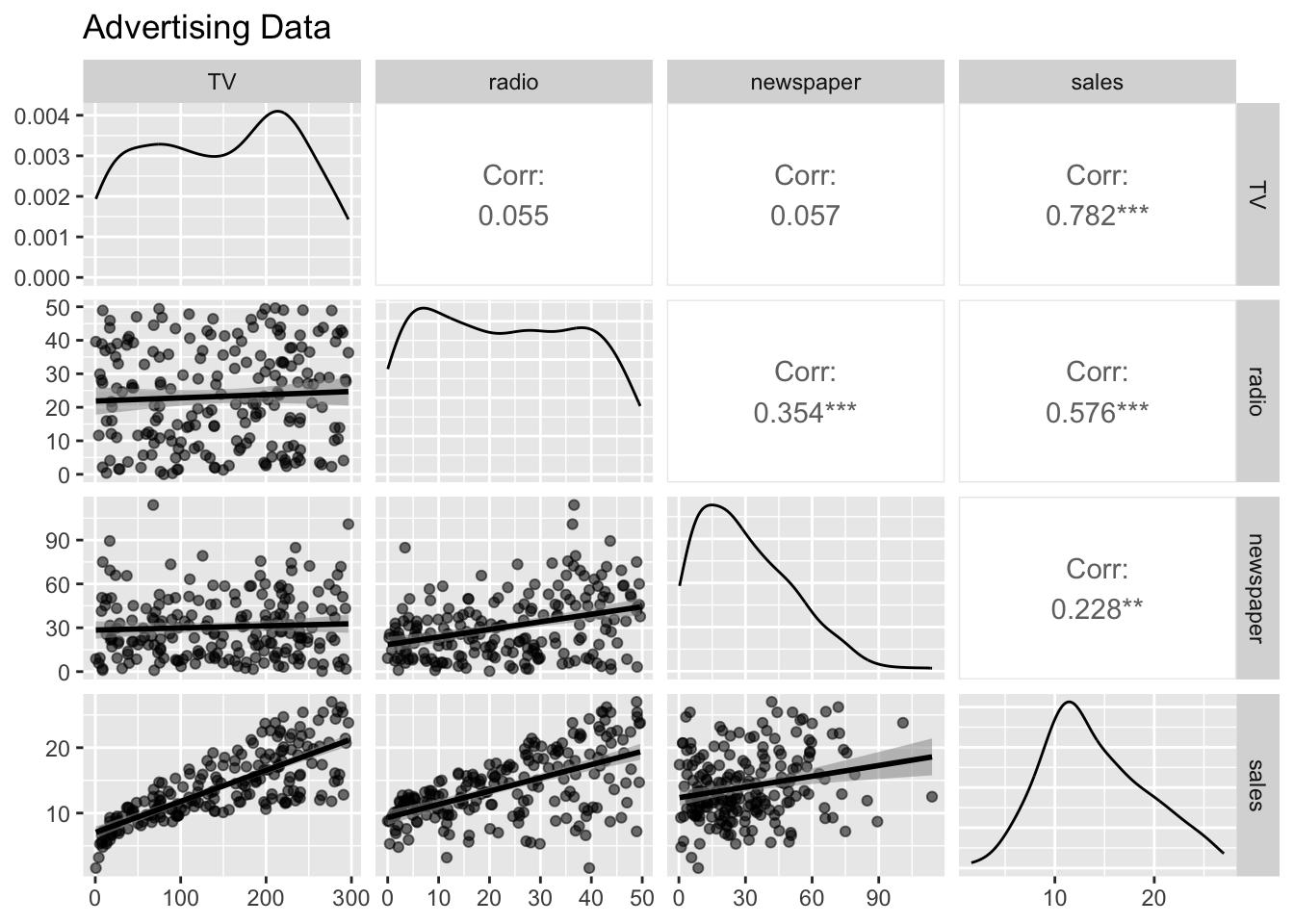

# Load the pandas libraryimport pandas as pd# Load numpy for array manipulationimport numpy as np# Load seaborn plotting libraryimport seaborn as snsimport matplotlib.pyplot as plt# Set font sizes in plotssns.set(font_scale =2)# Display all columnspd.set_option('display.max_columns', None)# Import Advertising dataAdvertising = pd.read_csv("../data/Advertising.csv", index_col =0)Advertising

Is there a relationship between advertising budget and sales?

How strong is the relationship between advertising budget and sales?

Which media contribute to sales?

How accurately can we predict future sales?

Is the relationship linear?

Is there synergy among the advertising media?

3 Simple linear regression vs multiple linear regression

In simple linear regression, we assume a model \[

Y = \underbrace{\beta_0}_{\text{intercept}} + \underbrace{\beta_1}_{\text{slope}} X + \epsilon.

\] For example \[

\text{sale} \approx \beta_0 + \beta_1 \times \text{TV}.

\] The lower left plot in the pair plot (R) displays the fitted line \[

\hat y = \hat \beta_0 + \hat \beta_1 \times \text{TV}.

\]

In multiple linear regression, we assume the model \[

Y = \beta_0 + \beta_1 X_1 + \beta_2 X_2 + \cdots + \beta_p X_p + \epsilon.

\] For example, \[

\text{sales} \approx \beta_0 + \beta_1 \times \text{TV} + \beta_2 \times \text{radio} + \cdots + \beta_3 \times \text{newspaper}.

\] We review the multiple linear regression below.

4 Estimation in multiple linear regression

We estimate regression coefficients \(\beta_0, \beta_1, \ldots, \beta_p\) by the method of least squares, which minimizes the sum of squared residuals \[

\text{RSS} = \sum_{i=1}^n (y_i - \hat y_i)^2 = \sum_{i=1}^n (y_i - \beta_0 - \beta_1 x_{i1} - \cdots - \beta_p x_{ip})^2.

\]

The minimizer \(\hat \beta_0, \hat \beta_1, \ldots, \hat \beta_p\) admits the analytical solution \[

\hat \beta = (\mathbf{X}^T \mathbf{X})^{-1} \mathbf{X}^T \mathbf{y}.

\] and we can make prediction using the formula \[

\hat y = \hat \beta_0 + \hat \beta_1 x_1 + \cdots + \hat \beta_p x_p.

\]

# sklearn does not offer much besides coefficient estimatefrom sklearn.linear_model import LinearRegressionX = Advertising[['TV', 'radio', 'newspaper']]y = Advertising['sales']lmod = LinearRegression().fit(X, y)lmod.intercept_

2.938889369459412

lmod.coef_# Score is the R^2

array([ 0.04576465, 0.18853002, -0.00103749])

lmod.score(X, y)

0.8972106381789522

import statsmodels.api as smimport statsmodels.formula.api as smf# Fit linear regressionlmod = smf.ols(formula ='sales ~ TV + radio + newspaper', data = Advertising).fit()lmod.summary()

OLS Regression Results

Dep. Variable:

sales

R-squared:

0.897

Model:

OLS

Adj. R-squared:

0.896

Method:

Least Squares

F-statistic:

570.3

Date:

Tue, 17 Jan 2023

Prob (F-statistic):

1.58e-96

Time:

08:51:15

Log-Likelihood:

-386.18

No. Observations:

200

AIC:

780.4

Df Residuals:

196

BIC:

793.6

Df Model:

3

Covariance Type:

nonrobust

coef

std err

t

P>|t|

[0.025

0.975]

Intercept

2.9389

0.312

9.422

0.000

2.324

3.554

TV

0.0458

0.001

32.809

0.000

0.043

0.049

radio

0.1885

0.009

21.893

0.000

0.172

0.206

newspaper

-0.0010

0.006

-0.177

0.860

-0.013

0.011

Omnibus:

60.414

Durbin-Watson:

2.084

Prob(Omnibus):

0.000

Jarque-Bera (JB):

151.241

Skew:

-1.327

Prob(JB):

1.44e-33

Kurtosis:

6.332

Cond. No.

454.

Notes: [1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

library(gtsummary)# Linear regressionlmod <-lm(sales ~ TV + radio + newspaper, data = Advertising)summary(lmod)

Call:

lm(formula = sales ~ TV + radio + newspaper, data = Advertising)

Residuals:

Min 1Q Median 3Q Max

-8.8277 -0.8908 0.2418 1.1893 2.8292

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.938889 0.311908 9.422 <2e-16 ***

TV 0.045765 0.001395 32.809 <2e-16 ***

radio 0.188530 0.008611 21.893 <2e-16 ***

newspaper -0.001037 0.005871 -0.177 0.86

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.686 on 196 degrees of freedom

Multiple R-squared: 0.8972, Adjusted R-squared: 0.8956

F-statistic: 570.3 on 3 and 196 DF, p-value: < 2.2e-16

We interpret \(\beta_j\) as the average effect on \(Y\) of a a one-unit increase in \(X_j\), holding all other predictors fixed.

a regression coefficient \(\beta_j\) estimates the expected change in \(Y\) per unit change in \(X_j\), with all other predictors held fixed. But predictors usually change together!

“Data Analysis and Regression”, Mosteller and Tukey 1977

Only when the predictors are uncorrelated (balanced or orthogonal design), each coefficient can be estimated, interpreted, and tested separately.

In other words, only in a balanced design, the regression coefficients estimated from multiple linear regression are the same as those from separate simple linear regressions.

Claims of causality should be avoided for observational data.

6 Some important questions

6.1 Goodness of fit

Question: Is at least one of the predictors \(X_1, X_2, \ldots, X_p\) useful in predicting the response?

We can use the F-statistic to assess the fit of the overall model \[

F = \frac{(\text{TSS} - \text{RSS})/p}{\text{RSS}/(n-p-1)} \sim F_{p, n-p-1},

\] where \[

\text{TSS} = \sum_{i=1}^n (y_i - \bar y)^2.

\] Formally we are testing the null hypothesis \[

H_0: \beta_1 = \cdots = \beta_p = 0

\] versus the alternative \[

H_a: \text{at least one } \beta_j \text{ is non-zero}.

\]

In general, the F-statistic for testing \[

H_0: \text{ a restricted model } \omega

\] versus \[

H_a: \text{a more general model } \Omega

\] takes the form \[

F = \frac{(\text{RSS}_\omega - \text{RSS}_\Omega) / (\text{df}(\Omega) - \text{df}(\omega))}{\text{RSS}_\Omega / (n - \text{df}(\Omega))},

\] where df is the degree of freedom (roughly speaking the number of free parameters) of a model.

lmod_null <-lm(sales ~1, data = Advertising)anova(lmod_null, lmod)

Analysis of Variance Table

Model 1: sales ~ 1

Model 2: sales ~ TV + radio + newspaper

Res.Df RSS Df Sum of Sq F Pr(>F)

1 199 5417.1

2 196 556.8 3 4860.3 570.27 < 2.2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

6.2 Model selection

Question: Do all the predictors help to explain \(Y\) , or is only a subset of the predictors useful?

For a naive implementation of the best subset, forward selection, and backward selection regressions in Python, interesting readers can read this blog.

6.2.1 Best subset regression

The most direct approach is called all subsets or best subsets regression: we compute the least squares fit for all possible subsets and then choose between them based on some criterion that balances training error with model size.

from abess.linear import LinearRegressionfrom patsy import dmatrices# Create design matrix and response vector using R-like formulaym, Xm = dmatrices('sales ~ TV + radio + newspaper', data = Advertising, return_type ='matrix' )lmod_abess = LinearRegression(support_size =range(3))lmod_abess.fit(Xm, ym)

LinearRegression(support_size=range(0, 3))

In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

However we often can’t examine all possible models, since there are \(2^p\) of them. For example, when \(p = 30\), there are \(2^{30} = 1,073,741,824\) models!

Recent advances make possible to solve best subset regression with \(p \sim 10^3 \sim 10^5\) with high-probability guarantee of optimality. See this article.

For really big \(p\), we need some heuristic approaches to search through a subset of them. We discuss three commonly use approaches next.

6.2.2 Forward selection

Begin with the null model, a model that contains an intercept but no predictors.

Fit \(p\) simple linear regressions and add to the null model the variable that results in the lowest RSS (equivalently the lowest AIC).

Add to that model the variable that results in the lowest RSS among all two-variable models.

Continue until some stopping rule is satisfied, for example when the AIC does not decrease anymore.

step(lmod_null,scope =list(lower = sales ~1, upper = sales ~ TV + radio + newspaper),trace =TRUE, direction ="forward" )

Start: AIC=661.8

sales ~ 1

Df Sum of Sq RSS AIC

+ TV 1 3314.6 2102.5 474.52

+ radio 1 1798.7 3618.5 583.10

+ newspaper 1 282.3 5134.8 653.10

<none> 5417.1 661.80

Step: AIC=474.52

sales ~ TV

Df Sum of Sq RSS AIC

+ radio 1 1545.62 556.91 210.82

+ newspaper 1 183.97 1918.56 458.20

<none> 2102.53 474.52

Step: AIC=210.82

sales ~ TV + radio

Df Sum of Sq RSS AIC

<none> 556.91 210.82

+ newspaper 1 0.088717 556.83 212.79

Call:

lm(formula = sales ~ TV + radio, data = Advertising)

Coefficients:

(Intercept) TV radio

2.92110 0.04575 0.18799

6.2.3 Backward selection

Start with all variables in the model.

Remove the variable with the largest \(p\)-value. That is the variable that is the least statistically significant.

The new \((p-1)\)-variable model is fit, and the variable with the largest p-value is removed.

Continue until a stopping rule is reached. For instance, we may stop when AIC does not decrease anymore, or when all remaining variables have a significant \(p\)-value defined by some significance threshold.

Backward selection cannot start with a model with \(p > n\).

step(lmod,scope =list(lower = sales ~1, upper = sales ~ TV + radio + newspaper),trace =TRUE, direction ="backward" )

Start: AIC=212.79

sales ~ TV + radio + newspaper

Df Sum of Sq RSS AIC

- newspaper 1 0.09 556.9 210.82

<none> 556.8 212.79

- radio 1 1361.74 1918.6 458.20

- TV 1 3058.01 3614.8 584.90

Step: AIC=210.82

sales ~ TV + radio

Df Sum of Sq RSS AIC

<none> 556.9 210.82

- radio 1 1545.6 2102.5 474.52

- TV 1 3061.6 3618.5 583.10

Call:

lm(formula = sales ~ TV + radio, data = Advertising)

Coefficients:

(Intercept) TV radio

2.92110 0.04575 0.18799

6.2.4 Mixed selection

We alternately perform forward and backward steps until all variables in the model have a sufficiently low \(p\)-value, and all variables outside the model would have a large \(p\)-value if added to the model.

step(lmod_null,scope =list(lower = sale ~1, upper = sale ~ TV + radio + newspaper),trace =TRUE, direction ="both" )

Start: AIC=661.8

sales ~ 1

Df Sum of Sq RSS AIC

+ TV 1 3314.6 2102.5 474.52

+ radio 1 1798.7 3618.5 583.10

+ newspaper 1 282.3 5134.8 653.10

<none> 5417.1 661.80

Step: AIC=474.52

sales ~ TV

Df Sum of Sq RSS AIC

+ radio 1 1545.6 556.9 210.82

+ newspaper 1 184.0 1918.6 458.20

<none> 2102.5 474.52

- TV 1 3314.6 5417.1 661.80

Step: AIC=210.82

sales ~ TV + radio

Df Sum of Sq RSS AIC

<none> 556.9 210.82

+ newspaper 1 0.09 556.8 212.79

- radio 1 1545.62 2102.5 474.52

- TV 1 3061.57 3618.5 583.10

Call:

lm(formula = sales ~ TV + radio, data = Advertising)

Coefficients:

(Intercept) TV radio

2.92110 0.04575 0.18799

6.2.5 Other model selection criteria

Commonly used model selection criteria include Mallow’s \(C_p\), Akaike information criterion (AIC), Bayesian information criterion (BIC), adjusted \(R^2\), and cross-validation (CV).

6.3 Model fit

Question: How well does the selected model fit the data?

\(R^2\): the fraction of variance explained \[

R^2 = 1 - \frac{\text{RSS}}{\text{TSS}} = 1 - \frac{\sum_i (y_i - \hat y_i)^2}{\sum_i (y_i - \bar y)^2}.

\] It turns out (HW1 bonus question) \[

R^2 = \operatorname{Cor}(Y, \hat Y)^2.

\] Adding more predictors into a model always increase \(R^2\).

From computer output, we see the fitted linear model by using TV, radio, and newspaper has an \(R^2=0.8972\).

The adjusted \(R_a^2\) adjusts to the fact that a larger model also uses more parameters. \[

R_a^2 = 1 - \frac{\text{RSS}/(n-p-1)}{\text{TSS}/(n-1)}.

\] Adding a predictor will only increase \(R_a^2\) if it has some predictive value.

The rooted squared error (RSE)\[

\text{RSE} = \sqrt{\frac{\text{RSS}}{n - p - 1}}

\] is an estimator of the noise standard error \(\sqrt{\operatorname{Var}(\epsilon)}\). The smaller RSE, the better fit of the model.

6.4 Prediction

Question: Given a set of predictor values, what response value should we predict, and how accurate is our prediction?

Given a new set of predictors \(x\), we predict \(y\) by \[

\hat y = \hat \beta_0 + \hat \beta_1 x_1 + \cdots + \hat \beta_p x_p.

\]

Under the selected model \[

\text{sales} \approx \beta_0 + \beta_1 \times \text{TV} + \beta_2 \times \text{radio},

\] how many units of sale do we expect with $100k budget in TV and $20k budget in radio?

95% Confidence interval: probability of covering the true \(f(X)\) is 0.95.

95% Predictive interval: probability of covering the true \(Y\) is 0.95.

Predictive interval is always wider than the confidence interval because it incorporates the randomness in both \(\hat \beta\) and \(\epsilon\).

7 Qualitative (or categorical) predictors

In the Advertising data, all predictors are quantitative (or continuous).

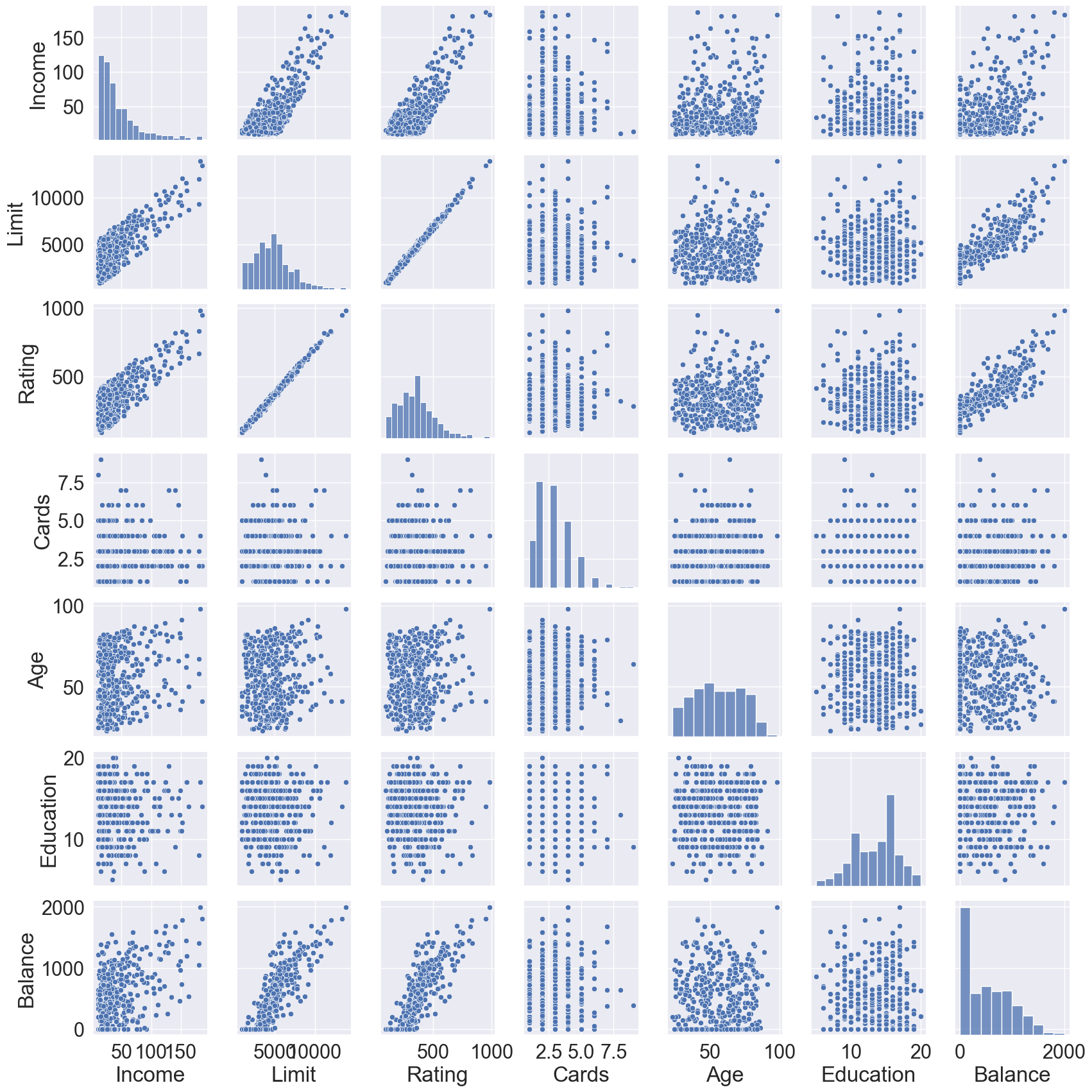

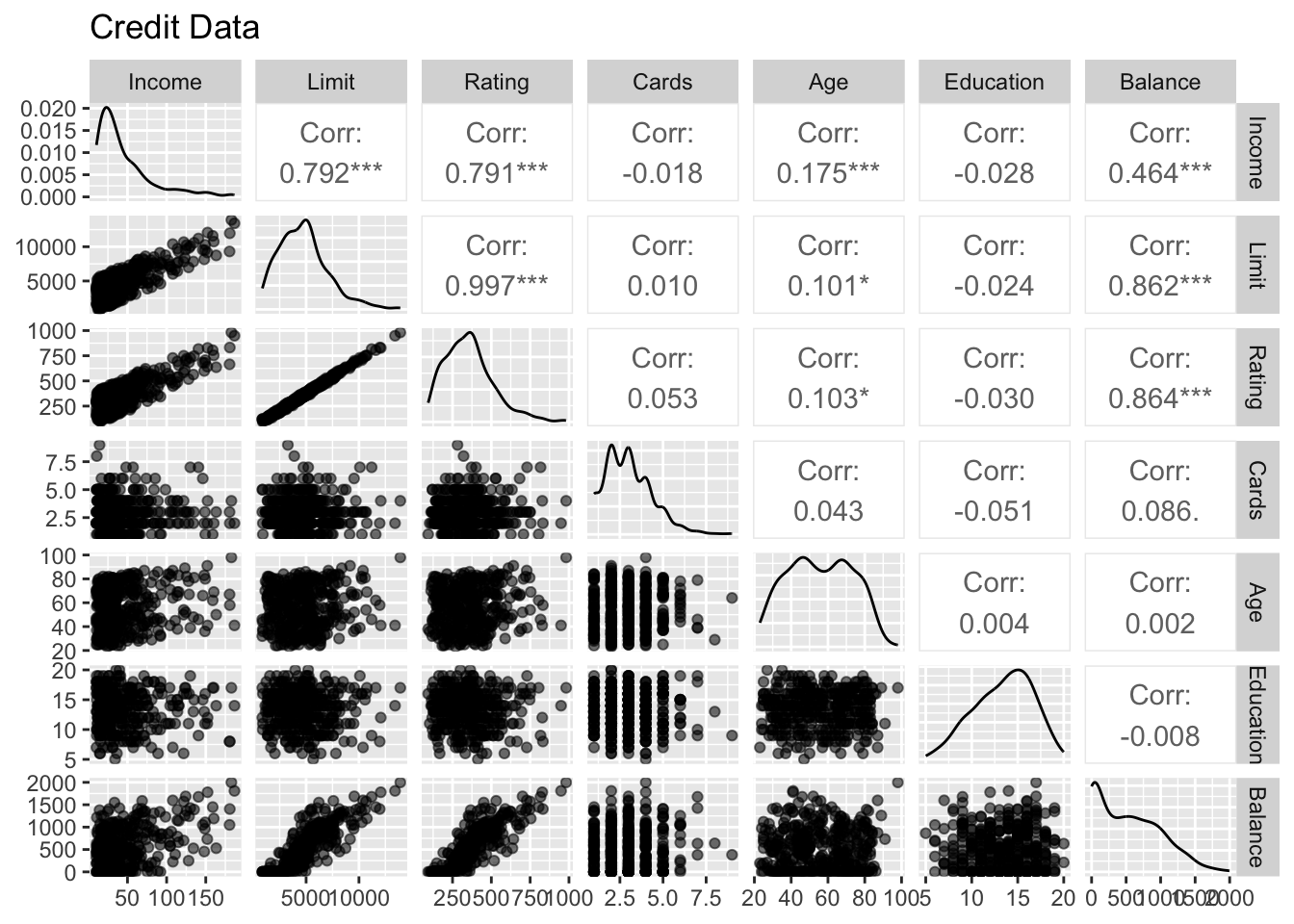

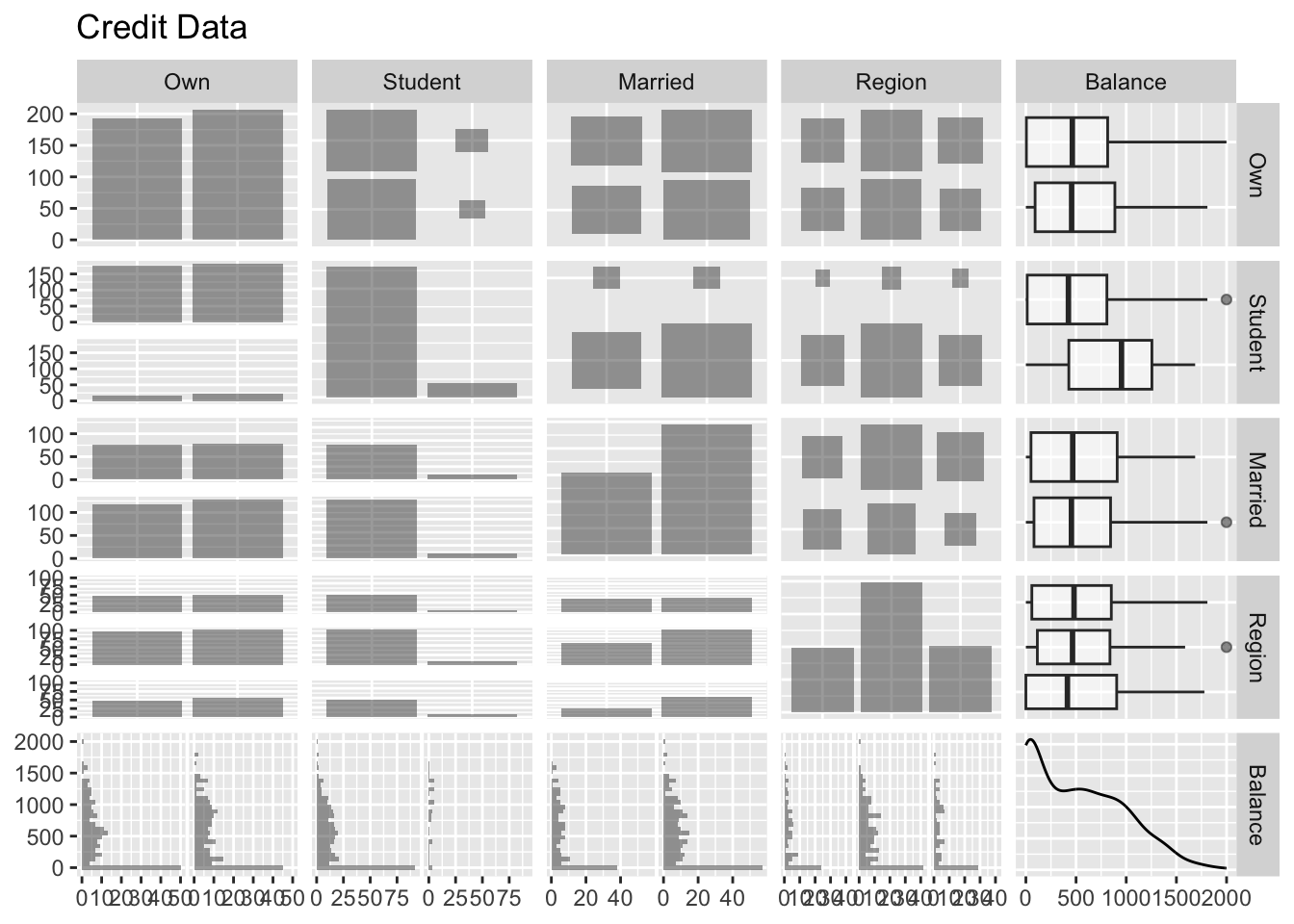

The Credit data has a mix of quantitative (Balance, Age, Cards, Education, Income, Limit, Rating) and qualitative predictors (Own, Student, Married, Region).

Income Limit Rating Cards Age Education Own Student Married \

0 14.891 3606 283 2 34 11 No No Yes

1 106.025 6645 483 3 82 15 Yes Yes Yes

2 104.593 7075 514 4 71 11 No No No

3 148.924 9504 681 3 36 11 Yes No No

4 55.882 4897 357 2 68 16 No No Yes

.. ... ... ... ... ... ... ... ... ...

395 12.096 4100 307 3 32 13 No No Yes

396 13.364 3838 296 5 65 17 No No No

397 57.872 4171 321 5 67 12 Yes No Yes

398 37.728 2525 192 1 44 13 No No Yes

399 18.701 5524 415 5 64 7 Yes No No

Region Balance

0 South 333

1 West 903

2 West 580

3 West 964

4 South 331

.. ... ...

395 South 560

396 East 480

397 South 138

398 South 0

399 West 966

[400 rows x 11 columns]

# Visualization by pair plotsns.pairplot(data = Credit)

# A tibble: 400 × 11

Income Limit Rating Cards Age Education Own Student Married Region

<dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <fct> <fct> <fct> <fct>

1 14.9 3606 283 2 34 11 No No Yes South

2 106. 6645 483 3 82 15 Yes Yes Yes West

3 105. 7075 514 4 71 11 No No No West

4 149. 9504 681 3 36 11 Yes No No West

5 55.9 4897 357 2 68 16 No No Yes South

6 80.2 8047 569 4 77 10 No No No South

7 21.0 3388 259 2 37 12 Yes No No East

8 71.4 7114 512 2 87 9 No No No West

9 15.1 3300 266 5 66 13 Yes No No South

10 71.1 6819 491 3 41 19 Yes Yes Yes East

Balance

<dbl>

1 333

2 903

3 580

4 964

5 331

6 1151

7 203

8 872

9 279

10 1350

# … with 390 more rows

By default, most software create dummy variables, also called one-hot coding, for categorical variables. Both Python (statsmodels) and R use the first level (in alphabetical order) as the base level.

# Hack to get all predictorsmy_formula ="Balance ~ "+"+".join(Credit.columns.difference(["Balance"]))# Create design matrix and response vector using R-like formulay, X = dmatrices( my_formula, data = Credit, return_type ='dataframe' )# One-hot coding for categorical variables X

# Fit linear regressionsm.OLS(y, X).fit().summary()

OLS Regression Results

Dep. Variable:

Balance

R-squared:

0.955

Model:

OLS

Adj. R-squared:

0.954

Method:

Least Squares

F-statistic:

750.3

Date:

Tue, 17 Jan 2023

Prob (F-statistic):

1.11e-253

Time:

08:51:57

Log-Likelihood:

-2398.7

No. Observations:

400

AIC:

4821.

Df Residuals:

388

BIC:

4869.

Df Model:

11

Covariance Type:

nonrobust

coef

std err

t

P>|t|

[0.025

0.975]

Intercept

-479.2079

35.774

-13.395

0.000

-549.543

-408.873

Married[T.Yes]

-8.5339

10.363

-0.824

0.411

-28.908

11.841

Own[T.Yes]

-10.6532

9.914

-1.075

0.283

-30.145

8.839

Region[T.South]

10.1070

12.210

0.828

0.408

-13.899

34.113

Region[T.West]

16.8042

14.119

1.190

0.235

-10.955

44.564

Student[T.Yes]

425.7474

16.723

25.459

0.000

392.869

458.626

Age

-0.6139

0.294

-2.088

0.037

-1.192

-0.036

Cards

17.7245

4.341

4.083

0.000

9.190

26.259

Education

-1.0989

1.598

-0.688

0.492

-4.241

2.043

Income

-7.8031

0.234

-33.314

0.000

-8.264

-7.343

Limit

0.1909

0.033

5.824

0.000

0.126

0.255

Rating

1.1365

0.491

2.315

0.021

0.171

2.102

Omnibus:

34.899

Durbin-Watson:

1.968

Prob(Omnibus):

0.000

Jarque-Bera (JB):

41.766

Skew:

0.782

Prob(JB):

8.52e-10

Kurtosis:

3.241

Cond. No.

3.87e+04

Notes: [1] Standard Errors assume that the covariance matrix of the errors is correctly specified. [2] The condition number is large, 3.87e+04. This might indicate that there are strong multicollinearity or other numerical problems.

lm(Balance ~ ., data = Credit) %>%tbl_regression() %>%bold_labels() %>%bold_p(t =0.05)

Characteristic

Beta

95% CI1

p-value

Income

-7.8

-8.3, -7.3

<0.001

Limit

0.19

0.13, 0.26

<0.001

Rating

1.1

0.17, 2.1

0.021

Cards

18

9.2, 26

<0.001

Age

-0.61

-1.2, -0.04

0.037

Education

-1.1

-4.2, 2.0

0.5

Own

No

—

—

Yes

-11

-30, 8.8

0.3

Student

No

—

—

Yes

426

393, 459

<0.001

Married

No

—

—

Yes

-8.5

-29, 12

0.4

Region

East

—

—

South

10

-14, 34

0.4

West

17

-11, 45

0.2

1 CI = Confidence Interval

There are many different ways of coding qualitative variables, measuring particular contrasts.

8 Interactions

In our previous analysis of the Advertising data, we assumed that the effect on sales of increasing one advertising medium is independent of the amount spent on the other media \[

\text{sales} \approx \beta_0 + \beta_1 \times \text{TV} + \beta_2 \times \text{radio}.

\]

But suppose that spending money on radio advertising actually increases the effectiveness of TV advertising, so that the slope term for TV should increase as radio increases.

In this situation, given a fixed budget of $100,000, spending half on radio and half on TV may increase sales more than allocating the entire amount to either TV or to radio.

In marketing, this is known as a synergy effect, and in statistics it is referred to as an interaction effect.

# Design matrix with interactiony, X_int = dmatrices('sales ~ 1 + TV * radio', data = Advertising, return_type ='dataframe' )# Fit linear regression with interactionsm.OLS(y, X_int).fit().summary()

OLS Regression Results

Dep. Variable:

sales

R-squared:

0.968

Model:

OLS

Adj. R-squared:

0.967

Method:

Least Squares

F-statistic:

1963.

Date:

Tue, 17 Jan 2023

Prob (F-statistic):

6.68e-146

Time:

08:52:03

Log-Likelihood:

-270.14

No. Observations:

200

AIC:

548.3

Df Residuals:

196

BIC:

561.5

Df Model:

3

Covariance Type:

nonrobust

coef

std err

t

P>|t|

[0.025

0.975]

Intercept

6.7502

0.248

27.233

0.000

6.261

7.239

TV

0.0191

0.002

12.699

0.000

0.016

0.022

radio

0.0289

0.009

3.241

0.001

0.011

0.046

TV:radio

0.0011

5.24e-05

20.727

0.000

0.001

0.001

Omnibus:

128.132

Durbin-Watson:

2.224

Prob(Omnibus):

0.000

Jarque-Bera (JB):

1183.719

Skew:

-2.323

Prob(JB):

9.09e-258

Kurtosis:

13.975

Cond. No.

1.80e+04

Notes: [1] Standard Errors assume that the covariance matrix of the errors is correctly specified. [2] The condition number is large, 1.8e+04. This might indicate that there are strong multicollinearity or other numerical problems.

lmod_int <-lm(sales ~1+ TV * radio, data = Advertising) summary(lmod_int)

Call:

lm(formula = sales ~ 1 + TV * radio, data = Advertising)

Residuals:

Min 1Q Median 3Q Max

-6.3366 -0.4028 0.1831 0.5948 1.5246

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6.750e+00 2.479e-01 27.233 <2e-16 ***

TV 1.910e-02 1.504e-03 12.699 <2e-16 ***

radio 2.886e-02 8.905e-03 3.241 0.0014 **

TV:radio 1.086e-03 5.242e-05 20.727 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.9435 on 196 degrees of freedom

Multiple R-squared: 0.9678, Adjusted R-squared: 0.9673

F-statistic: 1963 on 3 and 196 DF, p-value: < 2.2e-16

The results in this table suggests that the TV \(\times\) Radio interaction is important.

The \(R^2\) for the interaction model is 96.8%, compared to only 89.7% for the model that predicts sales using TV and radio without an interaction term.

This means that (96.8 - 89.7)/(100 - 89.7) = 69% of the variability in sales that remains after fitting the additive model has been explained by the interaction term.

The coefficient estimates in the table suggest that an increase in TV advertising of $1,000 is associated with increased sales of \[

(\hat \beta_1 + \hat \beta_3 \times \text{radio}) \times 1000 = 19 + 1.1 \times \text{radio units}.

\]

An increase in radio advertising of $1,000 will be associated with an increase in sales of \[

(\hat \beta_2 + \hat \beta_3 \times \text{TV}) \times 1000 = 29 + 1.1 \times \text{TV units}.

\]

Sometimes it is the case that an interaction term has a very small p-value, but the associated main effects (in this case, TV and radio) do not.

The hierarchy principle staties

If we include an interaction in a model, we should also include the main effects, even if the \(p\)-values associated with their coefficients are not significant.

The rationale for this principle is that interactions are hard to interpret in a model without main effects – their meaning is changed. Specifically, the interaction terms still contain main effects, if the model has no main effect terms.

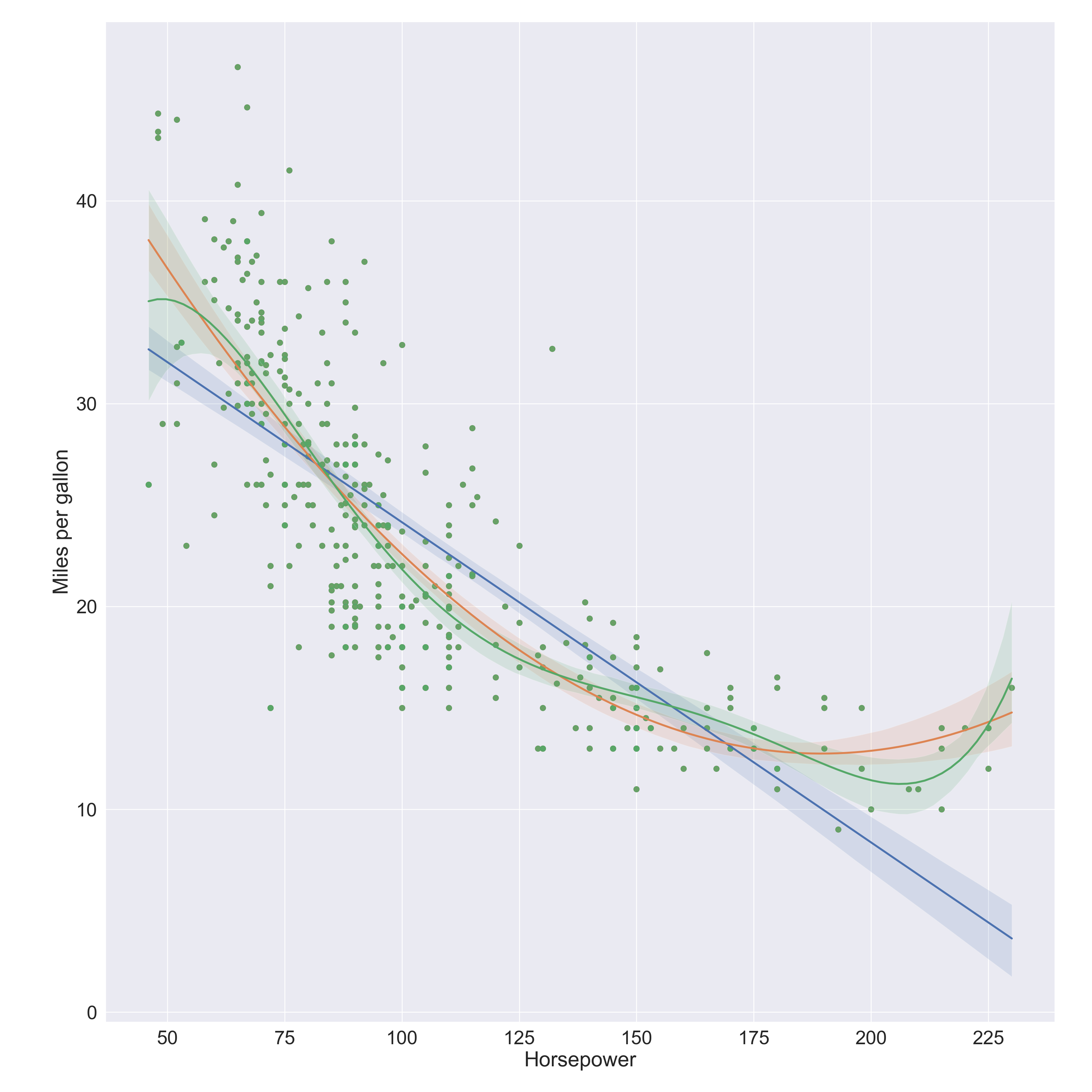

plt.clf()# Linear fitax = sns.regplot( data = Auto, x ='horsepower', y ='mpg', order =1 )# Quadratic fit sns.regplot( data = Auto, x ='horsepower', y ='mpg', order =2, ax = ax )# 5-degree fit sns.regplot( data = Auto, x ='horsepower', y ='mpg', order =5, ax = ax )ax.set( xlabel ='Horsepower', ylabel ='Miles per gallon')

# Linear fitlm(mpg ~ horsepower, data = Auto) %>%summary()

Call:

lm(formula = mpg ~ horsepower, data = Auto)

Residuals:

Min 1Q Median 3Q Max

-13.5710 -3.2592 -0.3435 2.7630 16.9240

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 39.935861 0.717499 55.66 <2e-16 ***

horsepower -0.157845 0.006446 -24.49 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.906 on 390 degrees of freedom

Multiple R-squared: 0.6059, Adjusted R-squared: 0.6049

F-statistic: 599.7 on 1 and 390 DF, p-value: < 2.2e-16

# Degree 2lm(mpg ~poly(horsepower, 2), data = Auto) %>%summary()

Call:

lm(formula = mpg ~ poly(horsepower, 2), data = Auto)

Residuals:

Min 1Q Median 3Q Max

-14.7135 -2.5943 -0.0859 2.2868 15.8961

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 23.4459 0.2209 106.13 <2e-16 ***

poly(horsepower, 2)1 -120.1377 4.3739 -27.47 <2e-16 ***

poly(horsepower, 2)2 44.0895 4.3739 10.08 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.374 on 389 degrees of freedom

Multiple R-squared: 0.6876, Adjusted R-squared: 0.686

F-statistic: 428 on 2 and 389 DF, p-value: < 2.2e-16

# Degree 5lm(mpg ~poly(horsepower, 5), data = Auto) %>%summary()

Call:

lm(formula = mpg ~ poly(horsepower, 5), data = Auto)

Residuals:

Min 1Q Median 3Q Max

-15.4326 -2.5285 -0.2925 2.1750 15.9730

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 23.4459 0.2185 107.308 < 2e-16 ***

poly(horsepower, 5)1 -120.1377 4.3259 -27.772 < 2e-16 ***

poly(horsepower, 5)2 44.0895 4.3259 10.192 < 2e-16 ***

poly(horsepower, 5)3 -3.9488 4.3259 -0.913 0.36190

poly(horsepower, 5)4 -5.1878 4.3259 -1.199 0.23117

poly(horsepower, 5)5 13.2722 4.3259 3.068 0.00231 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.326 on 386 degrees of freedom

Multiple R-squared: 0.6967, Adjusted R-squared: 0.6928

F-statistic: 177.4 on 5 and 386 DF, p-value: < 2.2e-16

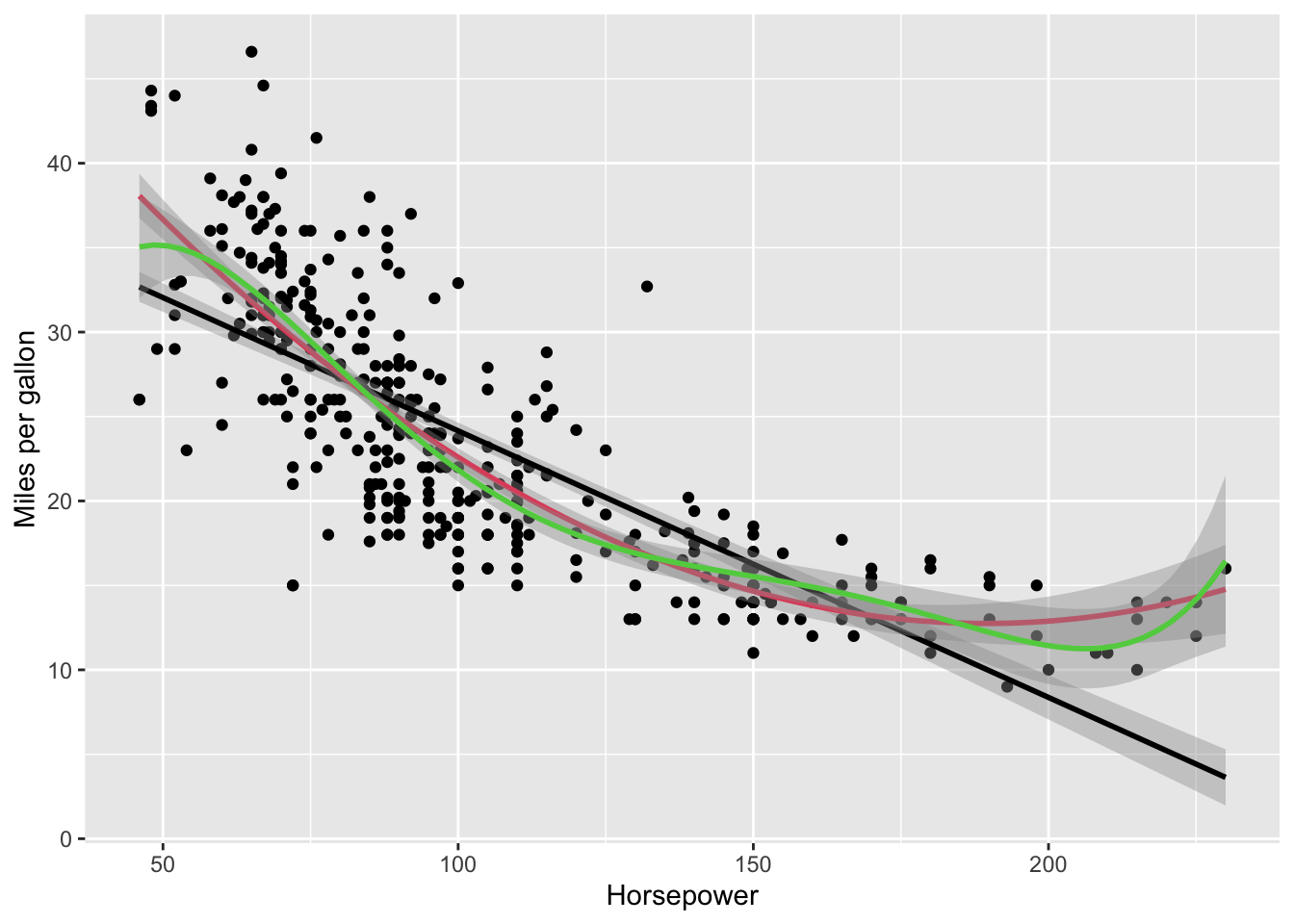

ggplot(data = Auto, mapping =aes(x = horsepower, y = mpg)) +geom_point() +geom_smooth(method = lm, color =1) +geom_smooth(method = lm, formula = y ~poly(x, 2), color =2) +geom_smooth(method = lm, formula = y ~poly(x, 5), color =3) +labs(x ="Horsepower", y ="Miles per gallon")

10 What we did not cover

Outliers.

Non-constant variance of error terms.

High leverage points.

Collinearity.

See ISL Section 3.3.3.

11 Generalizations of linear models

In much of the rest of this course, we discuss methods that expand the scope of linear models and how they are fit.

Classification problems: logistic regression, discriminant analysis, support vector machines.